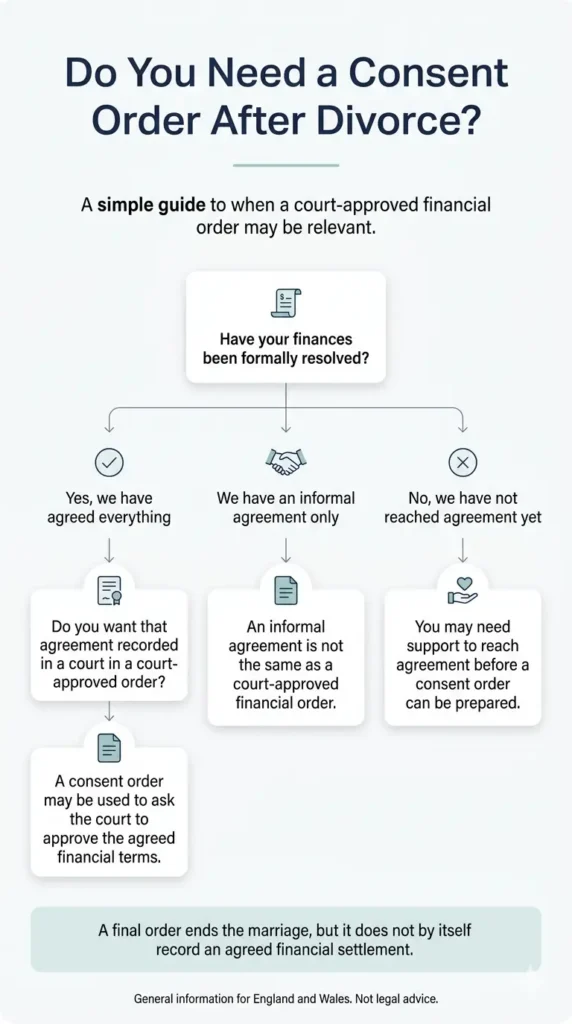

If you and your ex-partner have already reached an agreement about money or property after divorce, you may be wondering how to make that agreement legally binding. In England and Wales, that usually means applying for a consent order. GOV.UK explains that a consent order is used when you have agreed how to divide money and property and want the court to approve that agreement.

A lot of people also come across Form D81, and many are unsure how it fits into the process or whether they need it at all. There is also an important timing issue: GOV.UK says the court cannot approve a consent order before you have your conditional order (or decree nisi), and warns that if you want a legally binding arrangement for dividing money and property, you should apply for it before applying for the final order (or decree absolute), because there may be financial consequences, particularly for pensions.

What is a consent order?

A consent order is a proposed financial order that reflects an agreement already reached between you and your ex-partner. Instead of asking the court to decide a financial dispute after a hearing, you are asking the court to approve the terms you have both agreed. The court says that when you ask for approval, you and your ex-partner must draft a consent order, sign it, complete a statement of information form, and send the required documents and fee to the court.

This matters because reaching an agreement between yourselves does not automatically make it enforceable. A consent order is the step that asks the court to turn an agreed financial arrangement into a formal court order. Divorce finance guidance separates informal agreement from a court-approved financial order, which is why many people choose to formalise matters even when relations are relatively cooperative.

What is Form D81?

Form D81 is the statement of information used to support an application for a consent order in relation to a financial remedy. HMCTS says the purpose of the form is to help the court decide whether the financial and property arrangements you have made are fair.

In practice, Form D81 gives the judge a snapshot of both parties’ financial position and the terms of the agreement. That is why it is so important to complete it carefully and honestly. The form itself refers to matters such as dates of birth, relevant children, income, assets, liabilities, and whether a decree absolute or final order has been made.

Do I need a consent order after divorce?

Not everybody applies for a consent order, but it is often an important step where money, property, pensions, or ongoing financial claims need to be settled clearly. The court’s guidance on money and property after divorce says that if you want a legally binding arrangement for dividing finances, you need to apply to the court. That is the practical reason people often ask for a consent order even where they are already in agreement.

This is especially relevant where there are assets to divide, pension issues to deal with, or a wish to bring financial claims to an end as far as possible. The blog should be careful here: a consent order is not “mandatory” in every case, but it is often the route people use when they want legal certainty around an agreed settlement. That is a safer and more accurate way to explain it.

When should you apply for a consent order?

The court says it is usually simpler to ask the court to approve a consent order after you have your conditional order (or decree nisi), because the court cannot approve a consent order before that stage. The same guidance also says you should apply before your final order (or decree absolute), because leaving it until after final order can have financial consequences, particularly for pensions.

That timing point is one of the most important practical issues in this whole area. A lot of people assume that once the divorce is finished, they can sort out finances later with no downside. HMCT’s guidance makes clear that this can be risky, which is why consent-order timing should always be considered alongside the divorce timetable.

Should you get a consent order before the final order?

In many cases, yes. The court expressly says that if you want a legally binding arrangement for dividing money and property, you should apply for it before applying for the final order or decree absolute. It also says the consent order itself will only take effect after the final order or decree absolute is made.

That means two things can be true at once. First, the court normally wants the application for approval to come before final order. Second, the consent order does not take effect until final order is made. For readers, that is the key timing sequence to understand.

What happens if you divorce without a consent order?

If you divorce without putting a legally binding financial order in place, you may leave financial matters unresolved. HMCTS guidance does not say that every divorced person must get a consent order, but it does say that if you want a legally binding arrangement for dividing money and property, you need to apply to the court. That is why many people seek advice about a consent order even when they believe they have already agreed everything informally.

This does not mean every case will require the same solution. However, it does mean a blog on this topic should explain that divorce itself and financial finality are not always the same thing. The divorce ends the marriage; the financial order deals with agreed financial arrangements.

Can mediation help before a consent order?

Often, yes. Mediation can help separating couples discuss finances and reach proposals without asking the court to decide the outcome for them. If agreement is reached, the next step may then be to ask the court to approve that agreement through a consent order. That creates a natural bridge between mediation and the formal court approval process. Part 9 of the Family Procedure Rules governs financial remedy applications, while the court explains the separate practical steps for asking the court to approve a consent order.

At the same time, mediation and a consent order are not the same thing. Mediation may help people reach terms, but the consent order is the stage where the court is asked to approve the agreed financial arrangement. Form D81 supports that approval process by giving the court information about the parties’ financial circumstances.

How does this differ from Form A and Form E?

This is a different part of the divorce-finance journey. Form A and Form E are more closely associated with starting and managing a financial remedy application where finances are disputed or require formal disclosure. By contrast, consent orders and Form D81 sit more naturally in the agreed-settlement pathway. The courts separates Form A from the D81 consent-order material, and Part 9 of the Family Procedure Rules applies broadly to financial remedy applications.

A practical next step

If you have reached agreement about money or property after divorce, the next question is usually whether that agreement now needs to be turned into a legally binding order. In England and Wales, that is where the consent-order process and Form D81 commonly come in. GOV.UK’s guidance makes clear that timing matters, especially in relation to conditional order and final order.

For many people, the safest next step is to understand whether agreement has really been reached, whether mediation may still help refine the details, and whether the paperwork for a consent order is ready to go to court. That is often the point at which people ask about Form D81, legal drafting, and when to apply before final order.

Book a consultation regarding your divorce mediation.

0330 133 4858 Mon – Friday 9.00am – 5.00pm

Further Information: